Underwriters • Loan Officers • Processors • Mortgage Ops • CFOs

Master Cost Per Loan with Rapidio

Updated: · Rapidio

Author: Rapidio Editorial Team · Reviewed by: Senior Underwriter (10+ yrs) · About our review process

Introduction. In mortgage lending, cost per loan (CPL) defines your unit economics. This guide shows how to reduce CPL using Rapidio’s FlexStack Component System™: document classification and data extraction at $0, income calculation & eligibility, automated income verification, and AUS‑ready outputs for DU/LPA — with human‑in‑the‑loop QC.

Cost control

Typical SLA*

Redraws & callbacks

Table of contents

Why cost per loan matters

CPL is the backbone of margin control. Lowering CPL lifts profitability and resilience across rate cycles. Component‑based automation lets you pay only for what each file needs — no more “buffet pricing.”

The CPL formula

Use this simple model to baseline and track improvements:

CPL = (Fulfillment + Processing + UW + QC + Tech + Overhead) / Funded Loans

Track: SLA to income decision, redraw %, UW callbacks, approval rate, and staff hours per file.

7 levers to lower CPL

- Classification & IDP at $0: Document classification and extraction are included — eliminate re‑keying and vendor sprawl.

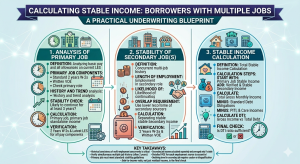

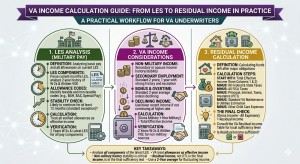

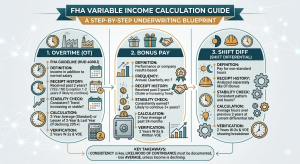

- Income calculation automation: Fannie Mae/Freddie Mac/FHA/VA packs, including self‑employed (Schedule C) and rental income (Schedule E, Borrower Rents).

- Bank statement cash‑flow: Use the online bank statement calculator for Non‑QM‑style workflows.

- Loan‑level activation: Turn components on per file — avoid paying when an AUS mortgage waiver applies.

- Exception‑only review: Let automation handle the routine; underwriters focus on judgment.

- Cleaner AUS handoff: AUS‑ready outputs for DU and LPA reduce callbacks and redraws.

- Training time ↓: Standardized worksheets and citations accelerate onboarding.

Rapidio Cost‑Per‑Loan Playbook

Step 1 — Baseline

Measure current CPL and time to income decision by product (FHA, VA, GSE). Identify top exception drivers.

Step 2 — Pilot income component

Activate on a slice of files. Compare before/after on SLA, redraw %, callbacks, and staff hours.

Step 3 — Expand to IDP

Add classification/extraction (included at $0) across paystubs, W‑2s, 1003s, bank statements, SSA‑1099, and tax returns.

Step 4 — Tighten AUS handoffs

Ensure outputs align to guideline packs; use income worksheets with rule citations for audits and manual underwriting.

Step 5 — Iterate & scale

Roll out by channel/branch. Monitor KPIs monthly; retire redundant tools to realize vendor savings.

Impact by role

- Underwriters: Less re‑keying; clearer income narratives; faster “approve/cond/deny.”

- Loan Officers & Brokers: Faster turn times; fewer conditions; better borrower experience.

- Ops Leaders & CFOs: Loan‑level cost control; scalable staffing; cleaner audits.

Security & compliance

Encryption in transit/at rest, role‑based access, audit logs, and guideline alignment (Fannie Mae, Freddie Mac, FHA, VA). Outputs retain provenance for exam readiness.

FAQs

Does Rapidio replace our LOS/POS?

Do you support self‑employed and rental income?

Is document classification really free?

How fast is the turnaround?

Start for free — 1 free calculation

Upload a file, choose your guideline pack (Fannie Mae, FHA, VA, Freddie Mac) and get a decisionable income result in minutes.

Try income calculation See pricing Book a 15‑min demo

*SLA varies by document type and complexity.