Underwriters • Loan Officers • Processors • Mortgage Brokers • CTOs

Asynchronous Awesomeness: The Epic Might of Component‑Based Mortgage Tech Stacks!

Updated: · Rapidio

Author: Rapidio Editorial Team · Reviewed by: Senior Underwriter (10+ yrs) · About our review process

If the boom of 2020 taught the industry anything, it’s that the mortgage tech stack must be flexible. One size can’t fit all, legacy systems can’t keep up, and expertise can’t be robotized. Looking to other industries that manage multiphase processes, we saw a model that enables asynchronous mortgage processing: the component‑based tech stack. Here’s why it’s better for modern loan manufacturing infrastructure.

Cost control

Parallel processing

Time‑to‑market

Table of contents

Never Overpay

End‑to‑end bundles are rigid and often bill for services you don’t need. For example, when you receive an income waiver and don’t require income calculation, a monolith still bakes that fee into the package—like paying for the whole buffet when all you want is a muffin. Components let you choose — and pay for — only the tech you actually use.

Loan Level Cost Control

Scale up or down by scenario and seasonality without blowing margins. Components activate per file, per need — so your IMB, credit union, or broker shop only incurs costs when value is delivered. This is how teams stay efficient during rate swings and seasonal spikes.

Modular Development (Asynchronous by design)

Loan manufacturing is a network of processes: income calculation, credit analysis, collateral (1004 appraisal), title, and closing. A component stack lets these run asynchronously and independently. Update or replace one module without risking the whole system — cutting development time and reducing risk.

On intake, your 1003 form and docs are classified and parsed. Then targeted components take over: Fannie Mae/Freddie/FHA/VA income calculation, income verification, or bank statement calculator for cash‑flow analysis. Results feed AUS (DU/LPA) or manual underwriting as needed.

Scalability & Flexibility

When volume surges, scale only the components that matter — no need to over‑provision an entire platform or rush‑hire. When it slows, scale back instantly. It’s infrastructure elasticity applied to mortgage workflows.

Maintenance & Upgrades

Traditional stacks turn upgrades into multi‑vendor marathons. With components, fixes and enhancements are isolated. Swap in a better extraction engine, refine an AI mortgage underwriting rule, or add a new calculator without downtime across your LOS/POS/CRM.

Future‑Proofing & Adaptability

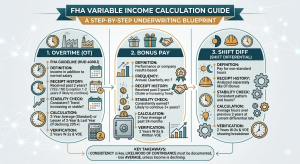

Because components are independent, you can adopt new capabilities—say, improved Fannie Mae income calculator logic or FHA variable income averaging—without re‑platforming. Your stack stays current with guideline shifts and technology breakthroughs.

Helpful references: Fannie Mae Selling Guide · FHA Handbook 4000.1

How Rapidio FlexStack Fits

- Income Calculation & Eligibility — Fannie Mae, Freddie Mac, FHA, VA with human‑in‑the‑loop QC

- Document Classification — included at $0 alongside data extraction

- Automated Income Verification — transcripts & validations

- Bank Statement Calculator — online cash‑flow analysis

- For Underwriters · For Lenders · For Brokers & Loan Officers

- Integration Partnerships — LOS/POS/CRM & middleware

Build to suit without months (or years) of customization. Launch faster, spend less, and keep margins intact.

Start for free — 1 free calculation

Try FlexStack with income calculation first. Upload a file, choose your guideline pack (Fannie Mae, FHA, VA, Freddie Mac) and get a decisionable result in minutes.