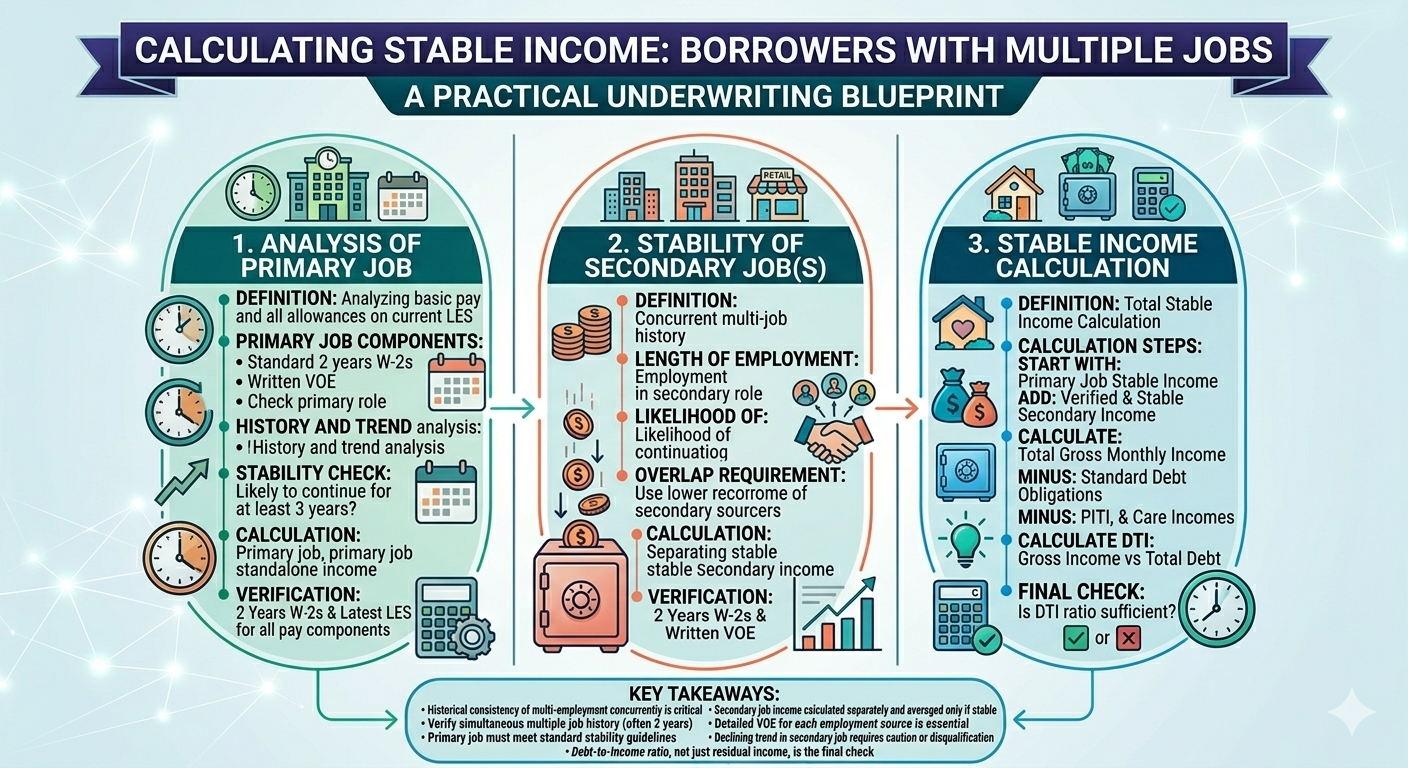

How to Calculate Stable Income for Borrowers with Multiple Jobs

Borrowers with multiple jobs are common - and they’re one of the fastest ways for a file to go suspense. The issue is rarely “two pay stubs.” The issue is stability: start dates, history windows, variable pay, job changes, hours, gaps, and how the income is combined. This guide gives a practical, repeatable approach to calculating stable qualifying income - and shows why standardizing this workflow reduces touches, suspense days, and cost per loan.

1. Why multi-job income is tricky

“Multiple jobs” creates underwriting complexity because each job can have different: start dates, pay types (salary/hourly/variable), hours consistency, and continuance likelihood.

Start-date risk

Second jobs are often recent. Recent = less history = higher condition risk.

Variable pay risk

Overtime/bonus/commission in job #2 often declines or is inconsistent.

Hours & fatigue risk

Underwriters want to see a believable pattern of sustained hours over time.

2. Step 1: classify each job (primary vs secondary)

Treat each job as its own income source first - then combine only what’s stable. A simple classification:

- Primary job: main employment, usually the strongest history and base pay.

- Secondary job: part-time/side employment that may need additional stability proof.

- Variable components: overtime/bonus/commission from either job should be treated separately.

3. Step 2: documents checklist (avoid suspense)

Use a consistent checklist so your processors don’t “discover” missing items after underwriting.

| Job Type | Minimum docs to start | Common add-ons that prevent suspense |

|---|---|---|

| Primary job | Recent pay stubs + W-2(s) | VOE if job change/new role or hours vary |

| Secondary job | Recent pay stubs + W-2(s) or year-end totals | VOE confirming start date, hours, and continuance |

| Variable pay (either job) | Pay stubs showing YTD + prior year(s) totals | Explanation for declines; additional history if recent |

4. Step 3: stability tests (history, gaps, hours, trend)

Before you include income from job #2, run a simple stability test:

4.1 History & start date

- How long has the borrower held job #2?

- Is there enough history to show a pattern (not just one pay stub)?

4.2 Hours consistency

- Are hours steady or swinging?

- Is it realistically sustainable alongside the primary job?

4.3 Trend check

- Is income increasing, stable, or declining compared to prior periods?

- If declining: do you have an explanation or should you use a conservative approach?

4.4 Gaps or job changes

- Any breaks in employment, role changes, or recent transitions that affect stability?

5. Step 4: calculation workflow (how to combine income)

Once each job passes stability checks, combine income using a clean structure:

- Calculate base income per job (salary or hourly × standard hours).

- Calculate variable income separately (overtime/bonus/commission) using history and run-rate logic.

- Apply conservative rule on declines (use the lower stable figure when trends conflict).

- Combine stable monthly amounts into total qualifying income.

- Document rationale + conditions for any unclear areas (start date, hours, variances).

6. Worked examples

Below are simplified examples to show the mechanics.

Example A: Primary salary + secondary part-time hourly

Separate each job and include only stable components.

Job #1 (Primary): Salary = $72,000/year Monthly base = 72,000 / 12 = $6,000 Job #2 (Secondary): Hourly $22/hr, 15 hrs/week Weekly = 22 * 15 = $330 Monthly (approx) = 330 * 52 / 12 = $1,430 Total qualifying (base) = 6,000 + 1,430 = $7,430/month

Secondary job still needs stability proof (start date, consistent hours). If recent, use conservative treatment and add conditions.

Example B: Secondary job with variable overtime declining

Use run-rate vs prior year and choose conservative figure.

Job #2 Overtime: Prior year overtime: $4,800 Current YTD overtime: $2,400 (as of month 9) Run-rate = 2,400 / 9 * 12 = $3,200 Conservative qualifying overtime = $3,200/year Monthly overtime = 3,200 / 12 = $267

If overtime decline is material, add a condition for explanation or use an even more conservative approach based on policy.

7. Smart Conditions checklist (copy/paste)

Use standardized conditions so multi-job files stop depending on “who reviewed it.”

- Secondary job history: Provide documentation to support history and stability of secondary employment (start date, consistent receipt).

- Secondary job hours: Provide VOE confirming hours and likelihood of continuance for secondary job.

- Variable income support: Provide sufficient history and documentation to support overtime/bonus/commission; explain any declining trend.

- Employment gaps: Provide explanation for any gaps or recent changes impacting stability of income.

- Documentation completeness: Provide missing pay stubs/W-2s required to support YTD and prior-year totals.

8. ROI: why this saves time and protects pull-through

Multi-job files are expensive when they aren’t standardized:

- More underwriter minutes spent reconciling jobs and pay types

- More conditions and suspense days due to missing stability proof

- More re-review loops because job #2 income changes midstream

- Higher cost per loan and lower pull-through when timelines slip

The ROI of a standardized multi-job workflow comes from reducing: UW minutes + touches + suspense days - and making the file predictable earlier.

Upload a loan with multiple jobs. Rapidio will return a guideline-ready income report plus Smart Conditions so your team can compare it to your current approach and avoid suspense surprises.