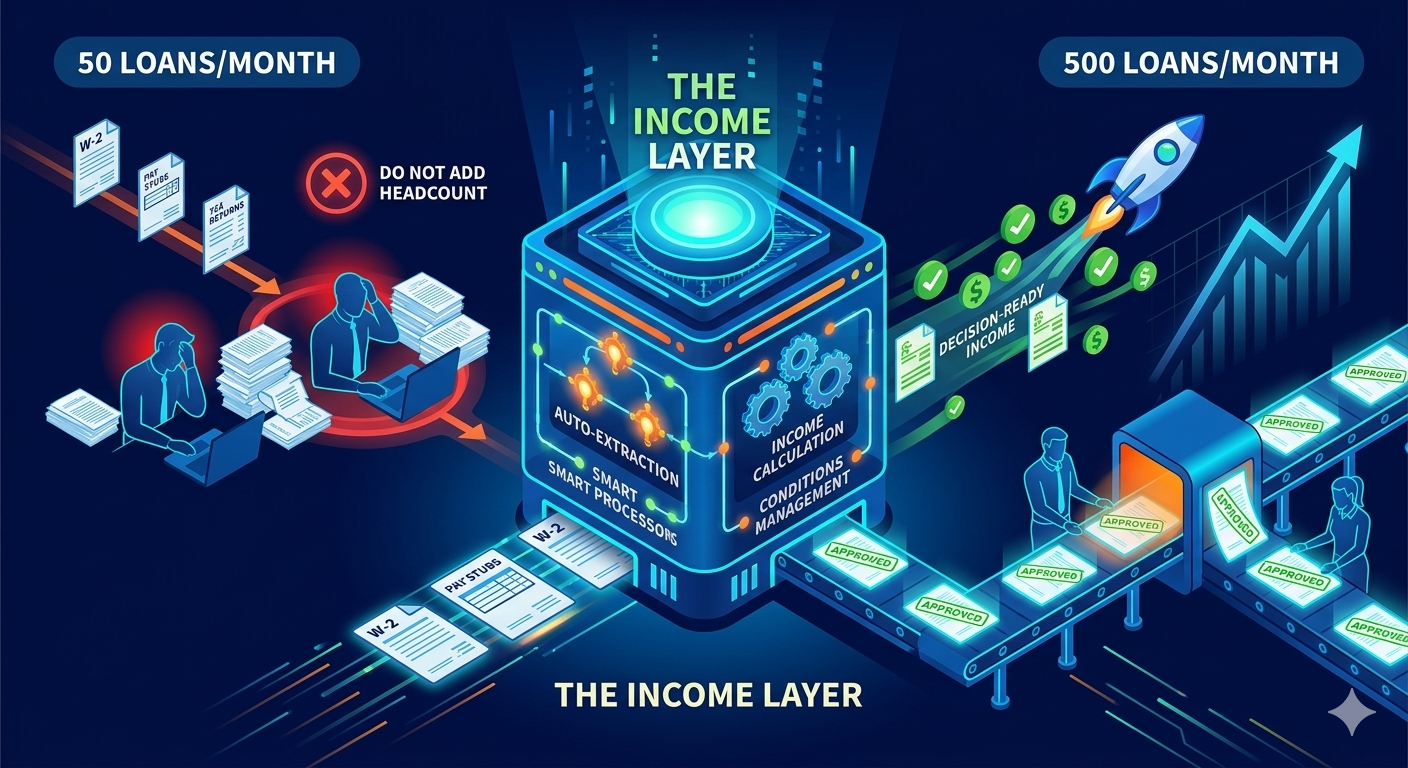

Scaling from 50 to 500 Loans per Month Without Adding Processors: The Income Layer

Most lenders assume scaling means hiring: more processors, more underwriters, more QC. But headcount scaling breaks fast - cost per loan rises, training becomes a bottleneck, and quality drifts across teams. The fastest way to scale throughput without scaling chaos is to standardize one thing that touches every loan: income + conditions. This is the “income layer.”

1. Why scaling from 50 to 500 breaks most operations

Going from 50 to 500 loans/month is not a “bigger version” of the same process. It’s a different operating system. Without standardization, three failure modes show up:

Training becomes the bottleneck

New hires take months to become productive, especially on complex income and conditions.

Variance explodes

Different processors and UWs treat income differently, creating rework and inconsistent decisions.

Cost per loan rises

More touches + more suspense + more re-reviews turns growth into margin compression.

2. What the “income layer” is (and why it’s the lever)

The income layer is a standardized, underwriting-grade service that sits across all channels (retail, broker, wholesale). It produces:

- Guideline-ready income calculations (FHA/VA/GSE/non-QM/reverse as needed)

- Smart Conditions to surface missing docs, gaps, declines, inconsistencies early

- One report format that underwriters, processors, and QC can all rely on

- Auditable rationale that reduces disputes and post-close issues

When income becomes standardized, the entire pipeline becomes more predictable - and predictability is what makes scale possible.

3. Where capacity is lost today (touches, suspense, rework)

Most lenders don’t run out of “people.” They run out of clean workflow. Capacity is lost through:

| Capacity Leak | What It Looks Like | Impact |

|---|---|---|

| Income rebuild | UW rebuilds income “just to be safe” | High-cost minutes; long queues |

| Re-review loops | Same file opened 2–4 times due to income changes | Touches per file rise fast with volume |

| Income-driven suspense | Missing docs discovered late | CTC delays; borrower/partner frustration |

| Variance across teams | Different interpretations across UWs/branches | QC defects; unpredictable approvals |

4. How the income layer enables 10x volume without 10x people

4.1 Processors stop being “spreadsheet builders”

In many shops, processors spend a surprising amount of time assembling income worksheets and chasing missing items. With the income layer, the workflow shifts:

- Processors use Smart Conditions as an upfront checklist.

- Income decisions become standardized - fewer debates and fewer corrections later.

- More of their time goes to movement, not math.

4.2 Underwriters validate instead of rebuild

This is the biggest scale lever. When UWs stop rebuilding income, they gain capacity without sacrificing quality.

4.3 Training becomes faster and more consistent

Instead of teaching every new hire “how we do income” through tribal spreadsheets, the engine becomes the standard:

- One report format, one condition language, one process.

- Faster onboarding and fewer “expert bottlenecks.”

4.4 Clean files reduce suspense and rework at scale

Suspense and re-review loops explode when volume increases. The income layer prevents that by catching issues earlier and standardizing how they’re cleared.

5. ROI: the math behind scaling without processors

Scaling ROI comes from minutes + touches + suspense days

Even conservative improvements compound quickly at 500 loans/month.

- Minutes: reduced UW income time per file

- Touches: fewer income-driven re-reviews

- Suspense: fewer income-driven suspense cases and shorter time in suspense

- Quality: fewer defects/cures and less policy drift across teams

Quick test: pick 20 loans → measure UW income minutes + re-review touches + suspense days → compare after the income layer.

6. Implementation plan: 2-week pilot → 30-day rollout

- Week 1–2 (Pilot): run 20–50 loans (include complex income) through Rapidio in parallel.

- Align outputs: confirm guideline packs and condition language with underwriting leadership.

- Define roles: processors clear Smart Conditions before UW; UWs validate, not rebuild.

- Week 3–4 (Rollout): standardize on the income report as “source of truth” for the pilot channel.

- Scale by channel: expand to remaining branches once KPIs improve.

7. KPIs to prove scale and protect quality

- Underwriter minutes spent on income per file

- Touches per file (income-driven re-reviews)

- Income-driven suspense rate + average days in suspense

- Time to initial UW decision

- Time from conditional approval to CTC

- Income-related defects/cures

- Cost per loan (minutes × loaded cost)

If these KPIs move together, you can scale volume while keeping quality stable - the definition of operational leverage.

Run a 2-week pilot on 20–30 loans with Rapidio. We’ll quantify savings in UW minutes, touches, and suspense days - and map what scaling looks like.