What a Fully Automated Income Workflow Looks Like (Step-by-Step Blueprint)

“Income automation” can mean anything from basic OCR to a full underwriting-grade engine. A truly automated income workflow does three things at scale: 1) produces guideline-ready income, 2) generates Smart Conditions early, and 3) reduces touches and suspense across the entire path to CTC. Here’s a practical blueprint you can implement without a massive re-platform.

1. What “fully automated income workflow” actually means

Fully automated doesn’t mean “no humans.” It means your team stops rebuilding income from scratch and starts operating with a standardized engine and outputs.

Automated intake

Docs flow in consistently (portal/API/LOS), not through ad hoc email chains.

Guideline-ready results

Income is calculated with the right guideline pack + auditable math.

Smart Conditions

Missing items and risks are flagged early, so they’re cleared before UW suspense.

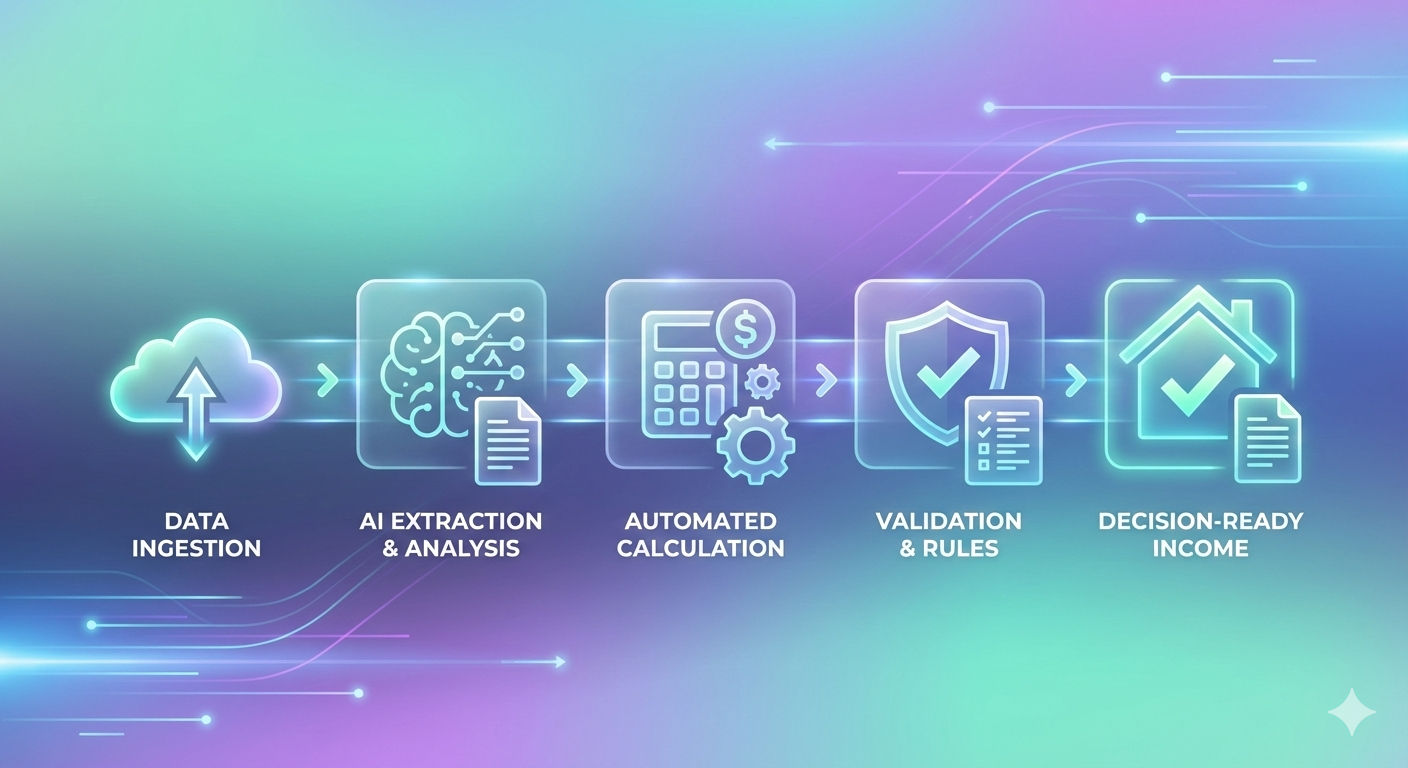

2. The operating model: intake → income engine → LOS

The most effective architecture is layered:

- Input: docs arrive from POS/LOS, broker portal, or secure upload

- Engine: income is calculated + Smart Conditions generated + QC applied

- Output: one standardized report (PDF + data) is returned to the loan file

- Feedback loop: exceptions and overrides are tracked to continuously tighten policy and training

This model standardizes income across branches and channels while keeping underwriting in control.

3. Step-by-step blueprint (8 steps)

Standardize how docs enter the workflow

Pick one primary intake path (portal or API). Make it the default for every channel.

- Goal: eliminate “missing docs by surprise” later

- ROI lever: fewer touches and fewer suspense cycles

Auto-classify income docs

Pay stubs, W-2s, tax returns, bank statements, SSA, pensions, LES - tagged and organized automatically.

- Goal: remove processor “doc stacking” time

- ROI lever: fewer minutes on non-value work

Extract granular fields (AI + QC)

Pull the details underwriting actually needs: YTD, base vs overtime/bonus, deposits, trends, dates.

- Goal: reduce manual reading and transcription

- ROI lever: fewer UW minutes per file

Apply the right guideline pack + overlays

Run calculations based on FHA/VA/GSE/non-QM/reverse logic and your credit policy overlays.

- Goal: eliminate “interpretation drift” across teams

- ROI lever: fewer re-reviews and fewer defects

Produce qualifying income with full math

Deliver borrower-level and source-level qualifying income with lookback windows and rationale.

- Goal: move UW work from “rebuild” to “validate”

- ROI lever: unlock underwriting capacity

Generate Smart Conditions immediately

Missing docs, gaps, declines, inconsistencies - surfaced early so processors can clear before UW.

- Goal: reduce suspense and late-stage chaos

- ROI lever: fewer suspense days, faster CTC

Return output to the loan file (PDF + data)

Attach the standardized income report and optionally push fields back into the LOS.

- Goal: one source of truth for UW/QC

- ROI lever: fewer touches and faster decisions

Track exceptions and improve continuously

Measure overrides, suspense causes, and income-driven delays. Use data to tighten policy and training.

- Goal: continuous reduction in variance and rework

- ROI lever: compounding cost-per-loan improvement

4. Where the ROI shows up (minutes, touches, suspense, defects)

Fully automated income workflows pay back in four places

This is how cost per loan drops while speed improves.

- Minutes: less UW time rebuilding income

- Touches: fewer re-reviews and back-and-forth loops

- Suspense: fewer income-driven suspense conditions and faster clearance

- Defects: fewer post-close cures due to standardized rationale

The fastest way to quantify ROI: pick 20 loans and measure UW income minutes, re-review touches, and suspense days before vs after.

5. KPIs to measure success

- Underwriter minutes spent on income per file

- Touches per file (income-driven re-reviews)

- Income-driven suspense rate + average days in suspense

- Time to initial UW decision

- Time from conditional approval to CTC

- Income-related defects/cures

6. Rollout plan: pilot → standard → scale

- Pilot on 20–50 loans (include complex income)

- UW validation of math transparency and condition language

- Standardize the report as “source of truth” for the pilot segment

- Scale by channel/branch once KPIs improve

This blueprint avoids the common failure mode: buying “AI,” then letting it sit on the side while teams keep using spreadsheets. The goal is to embed income automation into the operating model.

Choose 10–20 loans (include complex income). We’ll run them through Rapidio and help you compare time, touches, and conditions. You’ll see immediately where your workflow loses the most time - and what a fully automated income layer changes.