Vertical AI for Mortgage Income: Why Generic OCR/AI Isn’t Enough for Underwriters

Most “AI for documents” tools stop at text extraction. Underwriters don’t. They need guideline-ready income, Smart Conditions, and a calculation they can defend to investors. That’s where vertical AI for mortgage income comes in.

1. What lenders usually mean by “OCR” and “AI” today

When someone says “we already use AI for documents”, they usually mean one or more of the following:

- OCR engines that turn PDFs or images into text.

- Template-based extraction that looks for labels like “Gross Pay” and grabs the nearest dollar amount.

- Generic ML models trained on standard document layouts.

- A simple rules engine that pushes extracted fields into your LOS.

This is helpful for cutting some data entry on:

- W-2s and pay stubs

- Bank statements

- Standard income and ID documents

But notice what’s missing:

- Understanding of Fannie Mae, Freddie Mac, FHA, and VA rules.

- Any concept of stable vs. unstable income.

- Logic for averaging variable income over different time windows.

- Smart Conditions or a pre-UW file quality view.

- An audit trail that matches how underwriters actually think.

Generic OCR/AI is great at answering: “what does this line say?” Underwriters live in: “can I use this income, at what level, and under which guideline?”

2. What is vertical AI for mortgage income?

Vertical AI is AI built for one specific domain. It uses domain-specific data, rules, and workflows instead of generic models that try to do everything.

For mortgage income, that means going far beyond “read the pay stub.” A true vertical income engine should:

- Understand many document types: pay stubs, W-2s, 1099s, tax returns, bank statements, LES, pension and SSA letters, and more.

- Extract granular fields: YTD earnings, base vs overtime vs bonus, hours, rates, deposits, line items, and adjustments.

- Apply agency and product rules: FHA, VA, Fannie, Freddie, reverse, DSCR, and your overlays.

- Run calculation logic: correct averaging windows, stability checks, and include/exclude decisions per guideline.

- Output underwriter-ready results: qualifying income per borrower and per source, with full math and notes.

- Generate Smart Conditions for missing docs, gaps, declines, and inconsistencies.

- Integrate with your LOS/POS/QC so reports and data flow where your team works today.

3. Five reasons generic OCR/AI fails underwriters on income

3.1 It stops at “data” instead of “decision”

A generic tool might tell you: “Gross Pay YTD: $87,450.” An underwriter needs to know:

- Is this base, overtime, bonus, or commission?

- How many months of receipt do we have?

- Is income increasing, stable, or declining?

- What is the qualifying monthly income under the chosen guideline?

If your team still exports data to spreadsheets and manually rebuilds income calcs, you haven’t automated income — you’ve just moved the manual work to another screen.

3.2 It ignores agency guidelines and overlays

Agency rules are the core of the job, not an afterthought. You need correct treatment for:

- Bonus and commission income (Fannie vs Freddie differences).

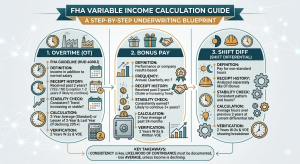

- Variable income, gaps and trends under FHA rules.

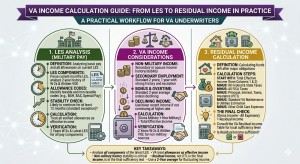

- Residual income and stability in VA loans.

- Product overlays for non-QM, DSCR, reverse, and more.

If guidelines are not encoded into the engine, someone on your team is still interpreting and recalculating. A vertical engine bakes those rules in, so outputs are guideline-aware by design.

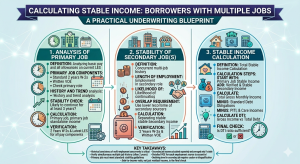

3.3 It breaks on messy, real-world borrowers

As soon as you leave the “one W-2 salaried” world, generic models struggle:

- Borrowers with multiple jobs and different start dates.

- Fluctuating overtime, shift differentials, and bonuses.

- Mix of W-2, 1099, and gig income.

- Self-employed with tax returns and bank statements.

- Seniors with Social Security, pensions, and part-time work.

Generic AI will still extract numbers — but it won’t decide what is stable, recognize declining trends, separate one-time from recurring income, or deliver a defensible final figure.

3.4 It can’t explain itself in “underwriter language”

When a file goes to suspense, investors and auditors ask:

- “How did you arrive at this income figure?”

- “Why did you include this overtime?”

- “Where is the 24-month history?”

Generic tools rarely provide a clear breakdown of each source, the averaging window, and the rationale. A vertical income engine outputs:

- All calculations and lookback periods.

- Which sources are included or excluded, and why.

- Conditions and notes in underwriter-friendly language.

3.5 It doesn’t fit your real operations

Common complaints about generic “document AI” in production:

- “LOS fields are populated, but UWs still don’t trust the numbers.”

- “Processors export everything to Excel anyway.”

- “It works for one channel, but not for brokers or wholesale.”

A vertical income engine is designed around how mortgage shops actually work: multiple channels, different doc quality, and the need for one consistent income view no matter where a file comes from.

4. What vertical AI for mortgage income looks like in practice

A modern vertical income engine typically follows this end-to-end path:

-

Ingest & classify

Any docs — PDFs, images, mobile photos, LOS exports — are uploaded and automatically classified into pay stubs, W-2s, 1099s, tax returns, bank statements, SSA letters, etc. -

Extract key fields (AI + rules + QC)

The engine pulls granular data (YTD earnings, hours, overtime, deposits, line items) and uses human-in-the-loop review for edge cases. -

Apply guideline logic

Specific guideline “packs” (Fannie, Freddie, FHA, VA, product overlays) determine which sources qualify, over which timeframe, and at what amount. -

Generate Smart Conditions

Missing docs, gaps, declines, inconsistent numbers, or high-risk patterns are converted into clear conditions before the file hits underwriting. -

Produce underwriter-friendly reports

Final qualifying income per borrower and source, full math, notes, and conditions are presented in one report. -

Sync with LOS / POS / QC

Reports and key fields are attached back to the loan file and can be used by QC, audit, and analytics.

For LOs, processors, and underwriters, this should feel like: “I upload docs and get qualifying income plus Smart Conditions in minutes, with math I can trust and explain.”

5. A simple checklist to evaluate income automation vendors

When you talk to any “AI document” vendor, ask:

- Mortgage-specific or generic? Do they serve many industries, or are they focused on lending and mortgage?

- Guideline packs? Can they show separate logic for Fannie, Freddie, FHA, VA, and specific products?

- Transparent calculations? Can underwriters see and adjust the math, or is it a black box?

- Smart Conditions vs simple flags? Are they giving UW-style conditions or generic “warnings”?

- Human-in-the-loop? What happens with messy, non-standard, or blurry docs?

- Time to value? How long from contract to the first live file? Can a small broker see value fast?

- Measurable ROI? Do they have real numbers on time saved, capacity gained, or suspense reduced?

6. Where Rapidio fits in the vertical AI landscape

Rapidio is built as a vertical AI engine for mortgage income and Smart Conditions, not a general-purpose document tool.

- Mortgage-only focus: We live inside FHA, VA, Fannie, Freddie, reverse and niche programs.

- From income to conditions: We don’t stop at a number — we surface the issues that will block your file.

- Human-in-the-loop QC: Every file is reviewed so your team receives 100% checked, guideline-ready output.

- Fast time to value: Brokers and lenders can sign up, upload their first file, and see a full income report in under 30 minutes.

If your team is still wrestling with spreadsheets, suspense conditions, and underwriter disputes after “going AI”, it’s a sign you don’t need more generic OCR — you need vertical AI for mortgage income.

Upload one complex loan — variable income, multiple jobs, or self-employed — and compare Rapidio’s income and Smart Conditions to your current process.