VA Income Calculation Guide: From LES to Residual Income in Practice

VA loans are not just about DTI - they’re about residual income. That’s why the LES (Leave and Earnings Statement) often becomes the make-or-break document: allowances, taxes, deductions, special pays, and obligations all impact what the borrower has left each month. This guide walks through a practical, underwriting-style method to calculate VA income from the LES - and how to avoid the conditions that slow VA files down.

1. Why VA income is different (DTI vs residual)

In many conventional files, DTI is the headline metric. VA underwriting adds an additional question: after paying taxes, debts, housing, and obligations - what does the borrower have left?

DTI answers

“Can the borrower afford the payment relative to income?”

Residual answers

“How much money is left for living expenses each month?”

LES matters because

It shows actual pay + allowances + deductions, not just a base salary line.

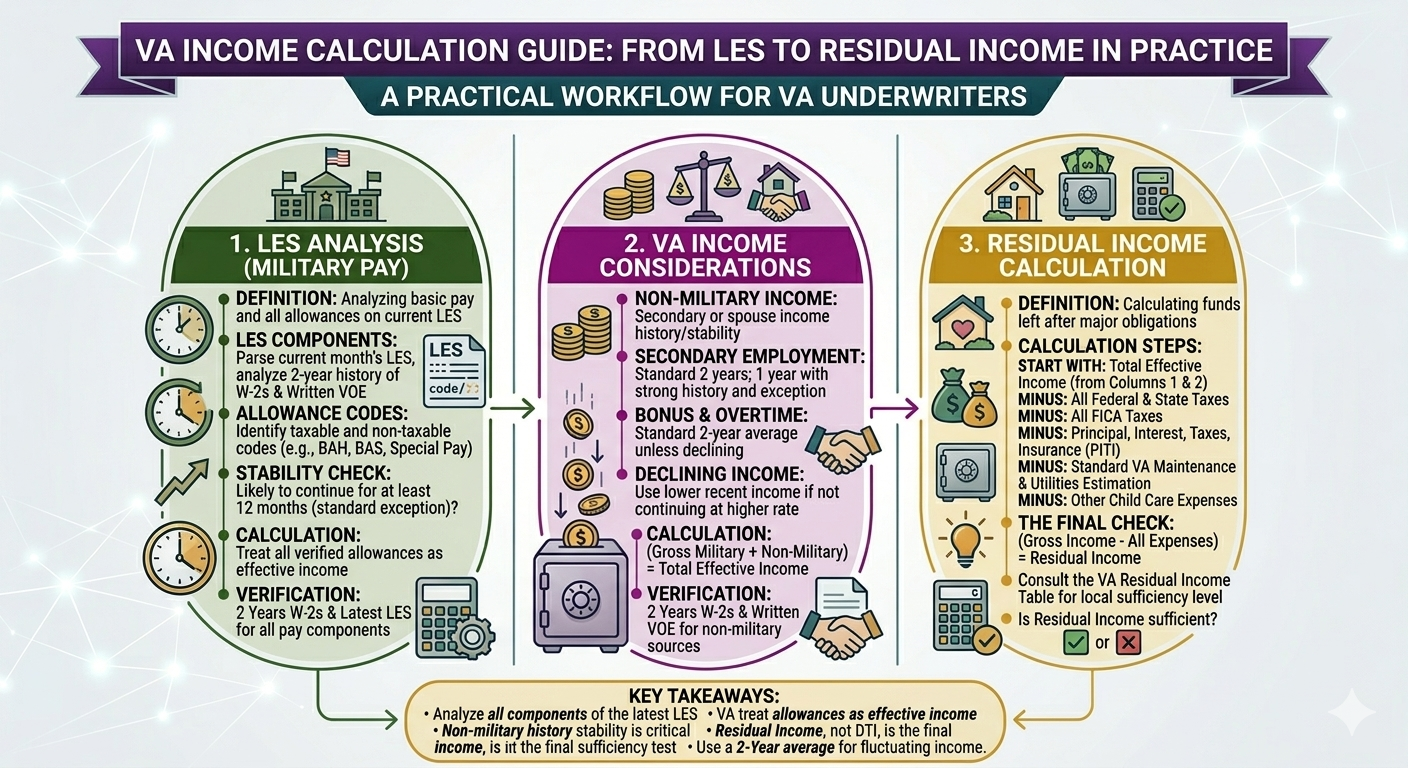

2. LES basics: what underwriters look for

An LES typically includes: base pay, special pay types, allowances, tax withholding, allotments, and other deductions. The underwriting challenge is separating what’s stable and continuing from what’s temporary or situational.

| LES Area | What It Represents | Underwriting Question |

|---|---|---|

| Base Pay | Core salary component | Is it stable and consistent with rank/time in service? |

| Allowances | Non-taxable or situational pay items | Which allowances are ongoing and usable? |

| Special/Other Pay | Various incentive or duty-based pays | Is it continuing or tied to temporary assignment? |

| Deductions | Taxes, insurance, contributions, obligations | Which deductions impact monthly net and residual? |

| Allotments | Directed payments (often recurring) | Are these debts/obligations that must be counted? |

3. Step 1: Identify stable income components

Start by splitting LES income into three buckets:

- Always stable: base pay (and stable, recurring pay components)

- Sometimes stable: certain special pays or allowances depending on circumstances

- Usually not stable: temporary assignment-based pay, one-time items, or pays that clearly end soon

Practical workflow

- Confirm base pay as the anchor income.

- List allowances and classify each as continuing vs temporary.

- List special pays and determine whether they have history and continuance.

- Document rationale for what you included/excluded (this prevents later disputes).

4. Step 2: Identify key deductions and obligations

Residual income depends on what’s left after obligations. From an ops perspective, the biggest time sinks come from missing or misunderstood deductions.

What to capture

- Taxes & withholding: core driver of net income

- Allotments: recurring directed payments (often obligations)

- Insurance / contributions: impact net cash available

- Other recurring deductions: anything that acts like a monthly obligation

5. Step 3: Calculate residual income (in practice)

The exact thresholds depend on family size, region, and other factors. But the practical calculation workflow is consistent across teams:

Residual Income - Practical Calculation Flow

Use your VA residual table for required minimums; this shows the mechanics.

1) Start with Gross Monthly Income (from LES components you included) 2) Subtract: - Estimated taxes / withholding (from LES or validated method) - Proposed housing expense (PITI + HOA + insurance as applicable) - Monthly debts/liabilities (credit report + recurring obligations) - Other recurring obligations shown on LES (e.g., allotments if applicable) 3) Result = Residual Income (monthly) 4) Compare residual income to the required VA minimum for: - Region - Family size - Loan amount / other factors per your policy

Tip: if residual is tight, the fastest way to avoid suspense is to ensure every income component and deduction is correctly classified and documented.

6. Common LES red flags that trigger conditions

These are the patterns that most often lead to rework or suspense:

- Allowances included without continuance support

- Special pay appears new (no history) or tied to a temporary assignment

- Allotments/deductions not explained or not reflected in liabilities

- Large swings in net pay month-to-month with no clear reason

- Deployment/temporary duty indicators impacting pay that may change

- Inconsistent LES dates or missing recent LES documentation

7. Smart Conditions checklist (copy/paste)

Standardize your VA conditions language so your files don’t depend on “who underwrote it.”

- LES history: Provide most recent LES statements required to support stable income and deductions.

- Allowance continuance: Provide documentation confirming which allowances are expected to continue.

- Special pay support: Provide history/confirmation for special pay items included in qualifying income.

- Allotment clarification: Provide explanation/documentation for LES allotments and whether they represent obligations.

- Residual income documentation: Provide residual income calculation worksheet showing income components, deductions, and comparison to required minimum.

- Net pay variance: Provide explanation for material changes in net pay or deductions.

8. ROI: why standardizing VA income saves real time

VA income calculations can be time-consuming - but the real cost comes from rework: when allowances are misclassified or deductions aren’t accounted for, teams reopen the file multiple times. That creates:

- Extra underwriter minutes per file

- More conditions and suspense days

- Longer time to CTC

- Higher cost per loan

The ROI of a standardized VA income workflow comes from reducing: UW minutes + touches + suspense days - and making approvals more predictable.

Upload a VA loan with an LES. Rapidio returns a guideline-ready income report plus Smart Conditions so your team can validate, not rebuild and avoid suspense surprises.