The Evolution of Automated Underwriting Systems in Mortgage Lending

From the first GSE-led AUS to today’s AI-powered engines, mortgage underwriting has shifted from manual checklists to real-time, data-driven decisions. Here’s how AUS evolved — and what’s next.

Speed

MinutesAccuracy

Guideline-trueScope

AUS + AIIntroduction

Mortgage underwriting has traveled a long road—from paper packets and manual overlays to automated decisioning and instant pre-quals. Automated Underwriting Systems (AUS) sit at the heart of this change, standardizing risk assessment and compressing cycle time for lenders and borrowers alike.

Pairing AUS with guideline-true income analysis and automated document classification is how modern teams reduce rework, shorten time-to-CTC, and lift pull-through.

The Genesis of Automated Underwriting

In the early 1990s, GSEs introduced the first AUS to bring consistency to borrower evaluation — centralizing credit, liabilities, DTI, LTV, and collateral rules into automated frameworks. Lenders gained standardized findings and clearer audit trails, while borrowers benefited from faster, more transparent decisions.

Key Milestones in AUS Development

- Early 1990s: First AUS launched by GSEs to unify underwriting standards and outputs.

- Late 1990s–2000s: Deeper risk models and broader data sources; tighter integration with LOS and credit.

- 2010s: Introduction of machine learning techniques and more granular policy logic; better treatment of variable income and layered risk.

- Today: AI-augmented AUS that incorporate document intelligence, real-time validations, and automated conditioning.

AI & ML: The New Chapter

Modern AUS increasingly leverage AI/ML to analyze high-volume, multi-format data — extending beyond bureau files to program-specific income rules and scenario nuance. With bank-statement income, W-2 & Self-Employed income, and QC signals flowing into one pipeline, lenders get consistent, guideline-aligned decisions.

What improves with AI-infused AUS

- Risk precision: better pattern detection for variable/declining income, layered obligations, and edge cases.

- Inclusivity: more informed views when traditional histories are thin — without sacrificing compliance.

- Cycle time: instant validation + automated conditions cut back-and-forth and redraws.

Current Trends in Mortgage Lending

Digital-first experiences now span application to closing. Lenders are standardizing on cloud workflows, real-time status, and API connectivity. AUS sits upstream, but downstream wins depend on the quality of inputs — especially income math and document integrity.

Digital-First AUS Pipelines

From pre-qual to clear-to-close, borrowers expect speed + transparency.

Compliance by Design

Automated conditions mapped to program rules reduce UW callbacks.

Green & Sustainable Lending

Emerging “green mortgages” and property-level data enter risk models.

The Future of Automated Underwriting

Expect tighter coupling between AUS, document AI, and program-specific income engines. Real-time validations, richer audit trails, and proactive “smart conditions” will make underwriting both faster and safer.

What to watch

- Personalized findings: overlays tuned per lender/investor while preserving auditability.

- Security: zero-trust patterns and granular PII controls baked into the pipeline.

- Ecosystems: lenders, fintechs, and partners co-owning a unified mortgage data layer.

Related Rapidio Resources

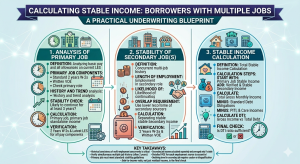

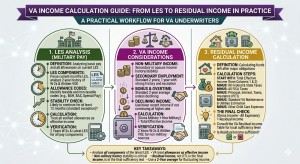

Guideline-True Income (W-2 & SE)

Underwriter-ready math with transparent assumptions and citations.

Learn moreBank Statement Calculator (12/24 mo)

Calculate eligible deposits in minutes—no spreadsheets.

Calculate incomeAutomated Document Classification

Stop sorting PDFs by hand—AI + human-verified accuracy.

See it in action