Big banks have entire teams building internal tools. Brokers don’t. Yet borrowers and Realtors compare everyone on the same two metrics: “How fast can you approve me?” and “Will this deal actually close?” Vertical AI for income and conditions is how smaller shops can finally answer both with confidence.

1. Why brokers are under pressure on speed & accuracy

Smaller broker shops live in a tougher world than big banks:

- You compete on speed of pre-approvals to win the borrower and the Realtor.

- You compete on accuracy because one bad deal damages your brand locally.

- You rarely have the budget for a large ops team or in-house tech department.

At the same time, income scenarios keep getting messier:

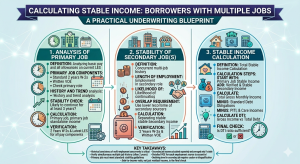

- Multiple jobs, gig work, and side businesses.

- Self-employed borrowers with layered entities.

- Seniors with pensions, Social Security, and part-time work.

Big lenders can throw people and internal tools at the problem. Brokers can’t. That’s exactly where vertical AI for income and Smart Conditions changes the game.

2. What “vertical AI for brokers” actually means

“AI” is everywhere now, but most of it is generic. Vertical AI means tools built specifically for mortgage lending, and even more specifically, for income decisions and conditions.

For brokers, a vertical AI income engine should be able to:

- Ingest any income docs you get from borrowers: pay stubs, W-2s, 1099s, tax returns, bank statements, LES, SSA letters.

- Extract the important details (YTD earnings, base vs overtime, bonuses, commissions, deposits).

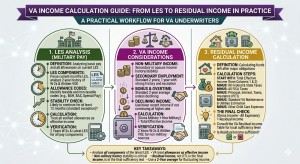

- Apply guideline logic for FHA, VA, Fannie, Freddie, non-QM, DSCR, reverse, etc.

- Calculate qualifying income per borrower with full math visible.

- Generate Smart Conditions that highlight missing docs, gaps, declines, and risks.

- Output a report you can share internally and with wholesale partners or lenders.

3. Where big banks really have the advantage (and where they don’t)

Big banks and large IMBs do have real advantages:

- Internal development teams building custom tools.

- Dedicated training programs for complex income.

- Specialized underwriting pods for self-employed and niche products.

But they also have real weaknesses that brokers can exploit:

- They move slowly. Changing a process can take months.

- They struggle to personalize service at the borrower and Realtor level.

- They often overcomplicate things and add friction for everyone.

A broker who uses vertical AI well can be:

- Faster at delivering accurate pre-approvals.

- Cleaner in the files they send to lenders and investors.

- Smarter in how they explain complex income to borrowers and partners.

That combination — speed, clean files, and human service — is exactly how brokers steal wins from bigger brands.

4. How vertical AI gives brokers big-bank speed

When a Realtor calls on a Saturday night and says, “Can you pre-approve this buyer by tomorrow?” you don’t have time for a full manual income analysis. But you also can’t afford to guess.

4.1 Faster pre-approvals with real numbers

A vertical AI engine lets you:

- Upload the borrower’s income docs in minutes.

- Get a guideline-aware income calculation back quickly.

- See Smart Conditions for what’s missing or uncertain.

That means you can issue pre-approvals based on a realistic income number, not a random guess, and you know exactly what you’ll need to clear before final approval.

4.2 Less back-and-forth when things get serious

Because income and conditions are standardized, when the file moves deeper into the process:

- You already have a clean list of conditions to clear with the borrower.

- You avoid “surprise” income changes when the lender’s underwriter looks at the file.

- You spend less time firefighting and more time originating.

That speed is noticeable to borrowers and Realtors — and they remember who got them approved quickly without drama.

5. How vertical AI gives brokers big-bank accuracy

Speed without accuracy is dangerous. The goal is both: get answers fast, and be able to stand behind them when the lender and investor review the file.

5.1 Guideline-consistent income decisions

With vertical AI, the income decision isn’t just your “best guess.” It’s based on:

- Embedded logic for FHA, VA, Fannie, Freddie, and non-QM programs.

- Clear treatment of overtime, bonus, commissions, and multiple jobs.

- Stability checks and lookback periods that match agency expectations.

This reduces the number of times a lender’s underwriter has to say, “We can’t use this income the way you calculated it.”

5.2 Smart Conditions that mirror underwriter thinking

A good income engine doesn’t just give you a number. It tells you:

- What’s missing (e.g., “Need 24 months of bonus history”).

- What looks risky (e.g., “Declining commission income; provide explanation”).

- Where you need more documentation (e.g., “Provide full tax returns due to self-employment”).

These Smart Conditions let you “think like an underwriter” before the file even reaches the lender. The result: fewer suspense conditions, fewer reworks, and more confidence in your approvals.

5.3 Consistency across your team

In a small shop, it’s common for each LO or processor to have their own way of doing income. Vertical AI replaces that with:

- One standard way to calculate income.

- One standard report everyone can read.

- One standard set of conditions to clear.

This consistency is a big part of what makes large lenders feel “safe” to work with — and brokers can have that same feeling without building it all themselves.

6. A simple vertical AI playbook for brokers

You don’t need a huge project plan. Here’s a simple way for brokers to start using vertical AI for income and conditions.

Step 1 – Start with your hardest files

Pick the scenarios that usually cost you the most time or anxiety:

- Self-employed borrowers.

- Multiple jobs and variable income.

- Borrowers over 55 with complex income sources.

Run those through an income engine and compare:

- Time to get a usable income figure.

- Clarity of the report and conditions.

- How often the lender’s underwriter changes the income later.

Step 2 – Make it part of your pre-approval ritual

Once you trust the output, build a simple rule for your shop, for example:

- “All self-employed pre-approvals go through the income engine.”

- “All loans above $X go through the income engine before we send them to the lender.”

This creates a consistent experience for your team and a visible upgrade in quality for your partners.

Step 3 – Use it as a selling point

Don’t keep it a secret. Use vertical AI as part of your pitch:

- To borrowers: “We use a dedicated income engine to make sure your file is accurate the first time.”

- To Realtors: “Our pre-approvals are stress-tested with the same logic lenders use.”

- To lenders: “Our files come with standardized income reports and Smart Conditions already cleared.”

This is how technology becomes not just an internal efficiency, but a differentiator in your local market.

7. How Rapidio is built specifically with brokers in mind

Rapidio is a vertical AI income & Smart Conditions engine that works especially well for brokers and small lending shops because:

- No heavy IT project: You can sign up, upload, and get reports from a secure portal.

- Guideline-aware logic: FHA, VA, Fannie, Freddie, reverse, and more baked in.

- Human-in-the-loop QC: Every file is checked so you get 100% reviewed output.

- Pay-per-use economics: Designed to make sense for brokers, not just mega-lenders.

- Shareable reports: Use the same income report internally and with your lender partners.

You don’t need a 20-person tech team to look like a sophisticated lender. You just need the right engine behind your income and conditions — and a clear story about how that helps your borrowers and partners.

Upload one complex borrower — self-employed, multiple jobs, or variable income — and compare Rapidio’s income report and Smart Conditions to your current process. See how vertical AI can help your brokerage compete on both speed and accuracy.